What if the story of declining loan officer numbers is just that — a story? If you’ve been around the mortgage industry awhile, you’ve surely heard of a sharp decline in licensed loan officer (LOs) numbers. Some reference a 50% drop in the LO population. Worse yet, other believe that license renewals are down 60%. These numbers — often presented with pride and alarm, depending on the voice — suggest that competition is thinning out dramatically.

But is that the reality? Recently released data from intelligence platform RETR, alongside my research conducted on the NMLS site, tells a very different story.

Breaking down the numbers

According to viral social media post last month, here are the numbers behind loan officer decline narrative:

- 2020: 688,327 licensed LOs

- 2024: 93,938 licensed LOs

At first glance, this paints a dire picture. However, digging deeper reveals a classic case of comparing apples to oranges. The 2020 figure reflects total licenses issued — meaning an LO licensed in five states is counted five times. Conversely, the 2024 number counts unique individuals, meaning LOs are counted based on individual status, instead of how many licenses they have in multiple states.

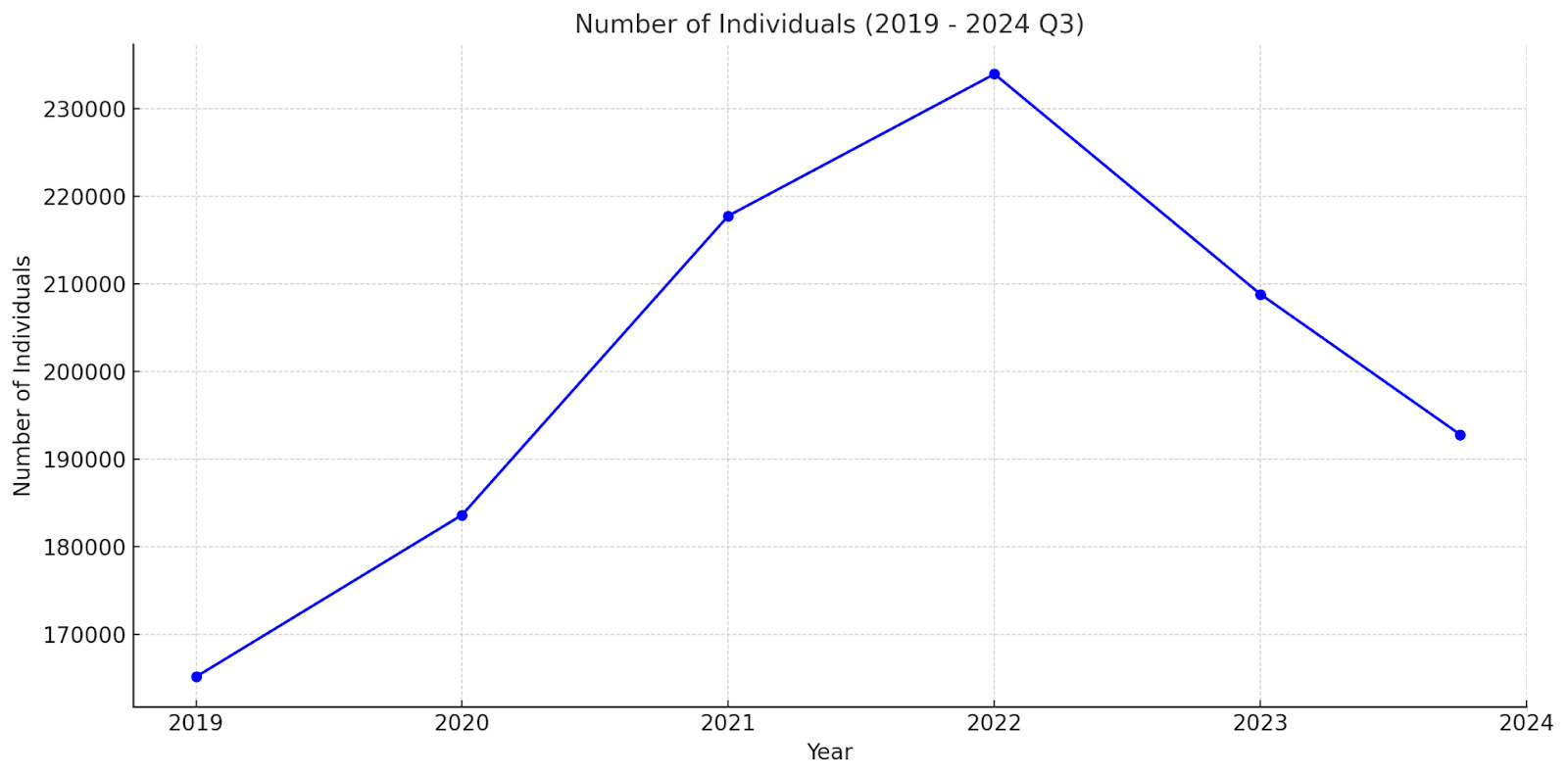

According to NMLS data, here is the real story behind LO numbers over the years (see Figure 1 below):

- 2019: 165,116 licensed loan officers

- 2022: Peak of 233,938 LOs (a 29% increase from 2019)

- 2024 Q3: 192,793 LOs (an 18% drop from the 2022 peak)

While there’s undoubtedly been a decline, it’s not quite as jaw-dropping as the figures floating around the internet. Moreover, RETR’s data on producing LOs — those who’ve actually closed a loan or two —shows a similar trend: a modest 10% drop, not the 50%-plus some suggest. That’s quite a different story — and one that’s slightly less apocalyptic.

The competitive landscape tells the bigger story

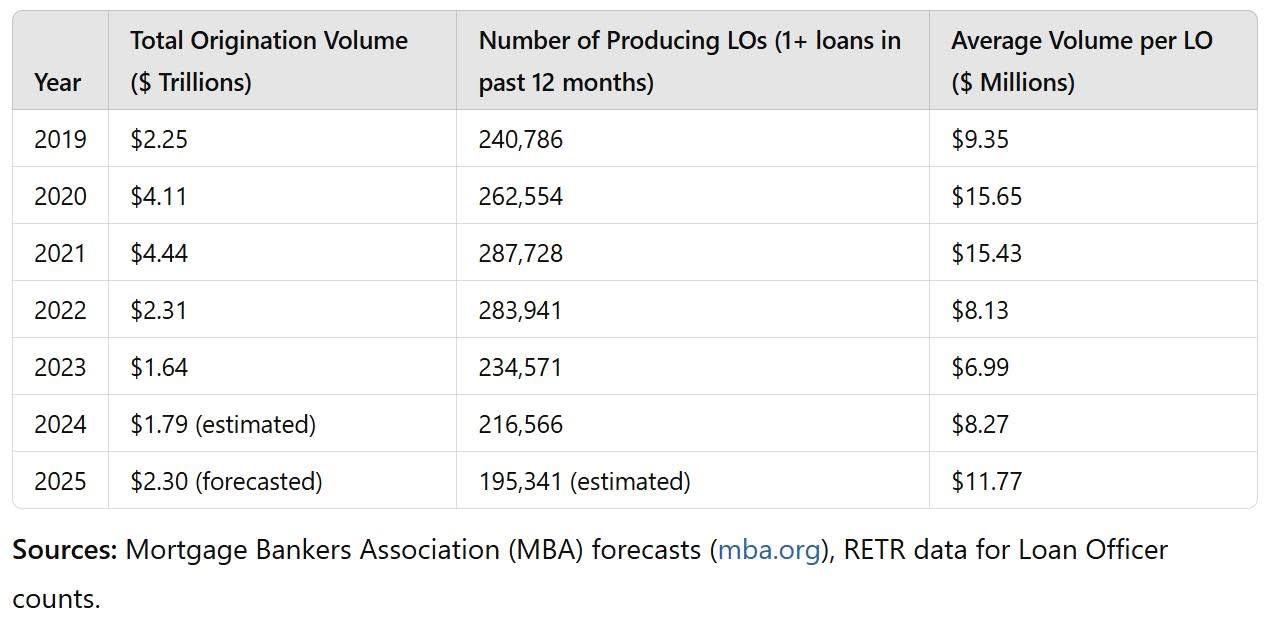

The bigger story lies in the competitive dynamics. While the number of LOs has declined, average volume per LO has fallen significantly since the market peak in 2020. According to data from the Mortgage Bankers Association (MBA) and RETR (see Table 1 below):

- In 2020, average volume per LO hit $15.65 million.

- By 2023, that number dropped to $6.99 million — a stark reflection of declining market volume and higher competition.

What is the good news? Projections for 2025 suggest a 40% increase in average volume per LO. That will be driven by rising origination volume and a slight continued decline in producing LOs.

A personal reflection to consider

For me, these insights were a wake-up call. I’d allowed the “LO decline” narrative to justify complacency. However, the data tells me otherwise. The competition is fierce, but opportunity is plentiful for those who adapt and stay proactive in the market. Whether you believe that you can or can’t, you’re right.

The numbers don’t lie. But they also don’t tell the whole story. Let this be a reminder: the future belongs to those who don’t just focus on surviving, but to those who are focused on innovating and growing all of the time.

See you at the top.

Michael McAllister

Founder/President of Empower LO

[email protected]